The art of successful investing comes down to diversification. The old adage; Don’t keep all of your eggs in one basket is sacrosanct. If the market is in a Risk on cycle, your growth stocks will flourish while your dividend stocks and bonds will lag behind and vice versa for Risk off. Since it’s unwise, and virtually impossible to time the market, having a well diversified portfolio allows you to take advantage of swiftly changing market cycles without losing your shirt.

With that in mind, P2P lending can add another layer of diversity to your overall investment strategy. Let’s take a look at P2P and see if it’s a good fit for your portfolio.

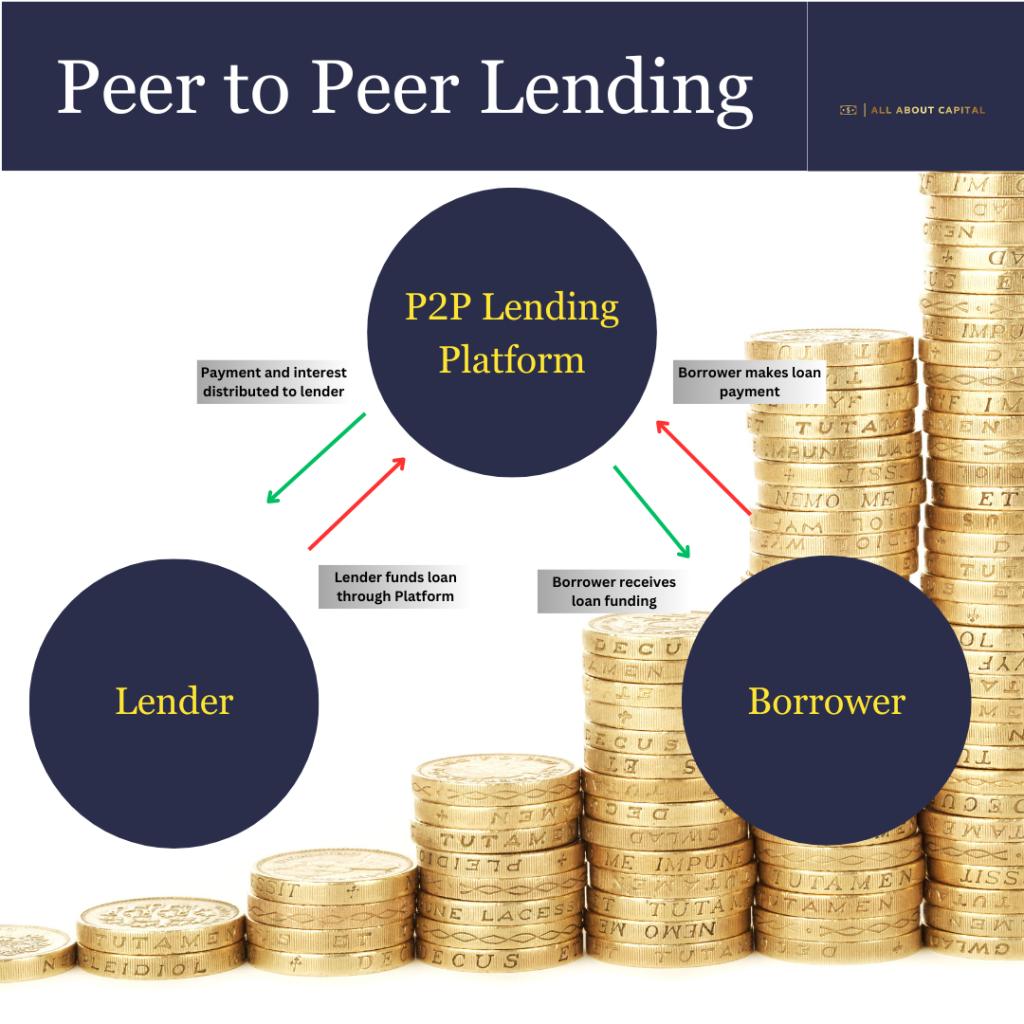

What is Peer to Peer Lending?

It’s exactly what it sounds like. Lending to your peers. More accurately, it’s a platform where people with excess money lend it to people who need it in return for interest payments. Pretty much exactly what a bank does, but with less red tape for the lendee and a bit more risk for the lender. We’ll discuss the risks and ways to reduce that risk later in the article.

So How Does it Work?

In order for P2P to work there must be a facilitator. Companies such as Prosper, Lending Club, and Upstart are a few examples of the leading platforms.

The lender will supply basic registration requirements and will then transfer the funds they wish to invest to the platform. Most facilitators will provide the lender with options on how they would like to distribute their funds to individual loans and what level of risk they are willing to accept.

The borrower will have to complete a more rigorous screening process such as credit check and proof of income. Once completed, the borrower will be assigned a risk profile and can then apply for a loan.

The facilitator acts as the middle man (for a small fee per transaction) and match up lenders to individual borrowers. The loans are divided into parts (minimum of $25) and offered out to lenders on their site. Once the loan has acquired enough to be fully funded, the proceeds of the loan are issued to the borrower.

As the borrower repays the loan, the principle and interest payment is divided between all the individual lenders on a monthly basis until the loan is paid in full.

What are the Risks/Rewards?

Let’s talk about risk. The primary risk to the lender is that these loans are UNSECURED. Meaning, the borrower does not need to provide collateral for these loans. The penalty for not repaying the loan will be a hit on their credit report. Now before you go running for the hills, the average default rate for P2P loans in the US is about 5%. That rate can vary drastically depending on what type of loans you choose to finance and the current economic climate.

Since I personally utilize the Prosper platform, I will talk about how they allow me to reduce the default rate on my loans.

- Choose a mix of loans that match your risk tolerance

- Limit the amount of money invested in each individual loan

- Specify the duration of loans that you are willing to fund

- Decide on what criteria you are willing to accept a loan

Risk Tolerance

Individual loans are graded based on the borrower’s credit rating, job history and income. In order to reduce risk, most facilitators allow lenders to invest in a variety of loan ratings. Loans with the best ratings have the lowest interest rates and vice versa for loans with poor ratings. I personally invest 90% of my funds into loans in the top rated brackets and invest the last 10% in the risker category. This allows me to maintain a relatively low default rate while also dabbling in the risky category to take advantage of the higher interest rates.

Limited Investment

Another way to reduce risk is to invest the minimum amount into each loan. I only invest $25 dollars into each loan thereby limiting my default exposure. For example, if you loaned a friend $1000 and he doesn’t pay you back, you’re out all of your money. But if you loan 40 friends $25 each, and 5% of them don’t pay you back, you only lose $50. You can easily absorb that loss with the interest the other 38 friends are paying you.

Loan Duration

The duration of a loan can last anywhere from 2 – 5 years. The length of time you choose should be based on your personal financial goals. It’s important to take into account that the money invested is LOCKED for the entire duration of the loan (unless the loan is paid back early). In my experience, loans under 3 years are usually of smaller value and have a lower default rate (but that’s NOT always the case).

Loan Criteria

Most facilitator platforms also give the lender the additional option to choose what criteria the borrowers have to meet in order for you to fund their loans. Some of the criteria are whether or not they need a cosigner, if they’ve had a delinquency on their credit report in a specific time frame, etc. Adding additional layers of criteria can greatly reduce the amount of loans available for you to choose from, but as always there are tradeoffs for reducing the amount of default risk.

In conclusion, P2P lending can be a great way to diversify your investment portfolio. if you’re willing to take some additional risk the rewards can be an additional stream of income with returns superior to those of money market accounts and treasury bonds. Be sure to only invest money that you will not need to have access to for the duration of your longest loans. And always keep your risk profile in mind when selecting loans to invest in.

Happy investing!